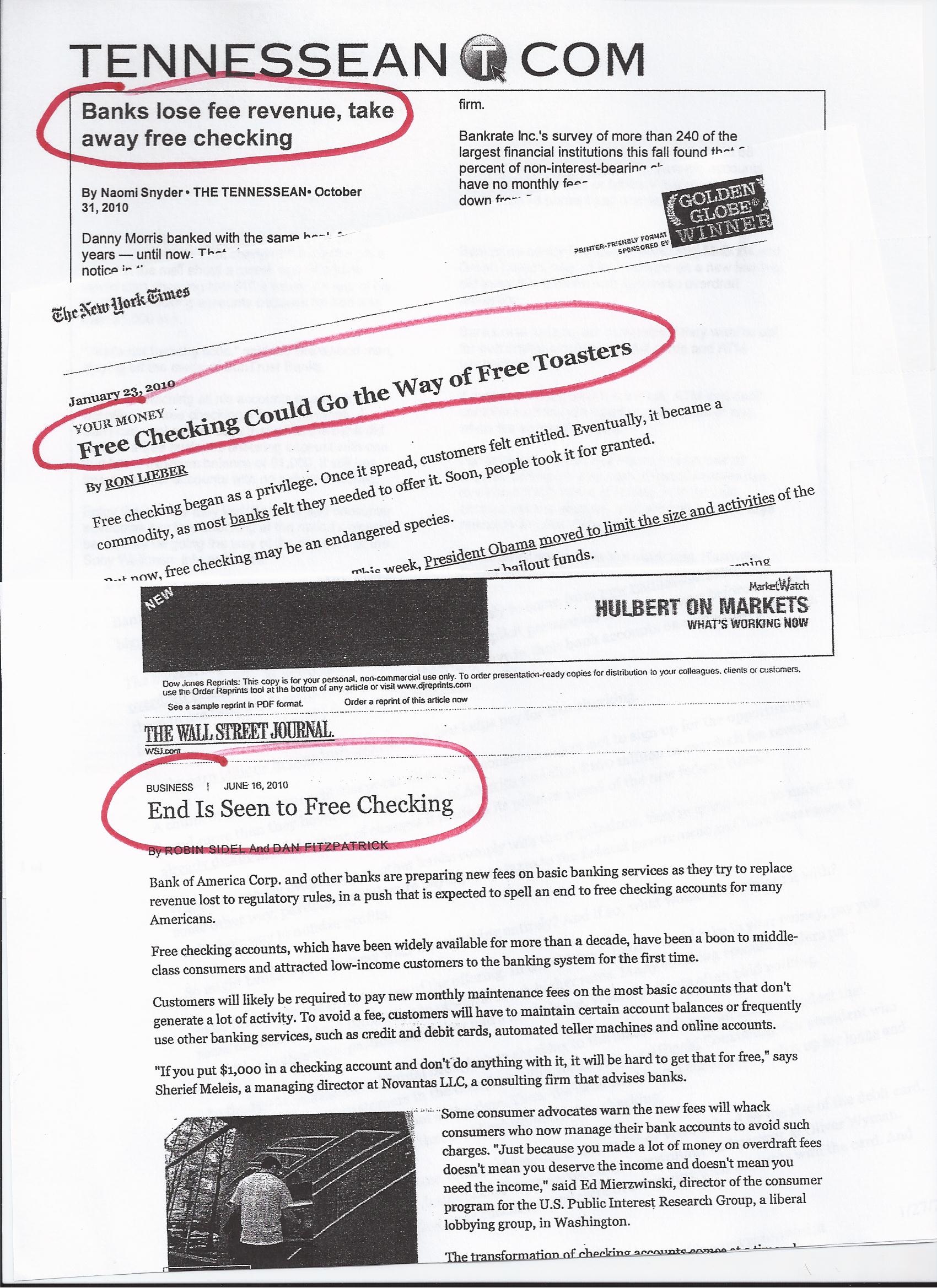

Attention financial writers – many of the articles over the past year about the pending death of free checking are based on erroneous information.

One of our goals with this site dedicated to the free checking account is to provide the truth about free checking. As a financial writer we trust you’ll visit this site when writing any articles about free checking or when free checking is mentioned. Should you have an inquiry that cannot be answered by one of the many articles on this site, please contact us immediately and we’ll provide the information to the extent possible.

As for information we’ve encountered in recent free checking articles, here are some examples of information that is wrong or misleading:

- The free checking account is on its way out, it’s dead.

- The free checking account was created or started by a major bank in Minnesota.

- The free checking account is unprofitable.

- The mega-banks have been offering free checking for years.

- Free checking was started by the big banks.

- Free checking attracts only the lower income consumer who keeps a low balance.

- Banks can’t survive if they continue offering free checking.

- Banks have to drop free checking because of loss of overdraft fee income, a reduction in debit card interchange fees, and predicted high compliance costs as a result of the Dodd-Frank legislation.

None of the information above is even remotely correct and should not be used when writing articles and blogs about the free checking account.

Free Checking is Alive and Well

About the only banks dropping free checking are the four mega-banks – Wells Fargo, Bank of America, Chase, and Citibank. Unfortunately, because of their combined market share and nationwide coverage, their actions dominate the media. Occasionally, another smaller bank will follow along because of the lemming instinct – if the big banks are dropping free checking, it must be the right course of action.

What isn’t being reported in the media are the thousands of smaller community banks and credit unions still offering free checking. Most of institutions have no plans to drop free checking – especially now. They now have a stronger competitive advantage over the mega-banks operating in their market areas.

The Free Checking movement was launched in 1982 in Lincoln, Nebraska

Free checking as we know it today started in Lincoln, Nebraska in 1982, with the launch of the Totally Free Checking and Free Gift marketing program. It was not a bank or credit union that created this unique account or marketing program – it was a direct mail vendor that specialized in marketing campaigns for small banks. So, in effect, free checking had its origins at hundreds of small, community banks across America.

Free checking as we know it today started in Lincoln, Nebraska in 1982, with the launch of the Totally Free Checking and Free Gift marketing program. It was not a bank or credit union that created this unique account or marketing program – it was a direct mail vendor that specialized in marketing campaigns for small banks. So, in effect, free checking had its origins at hundreds of small, community banks across America.

It wasn’t until the late 1990s that the four mega-banks and other large banks began offering free checking. And they did so strictly as a competitive or defensive move. They were among the last banks to offer free checking and first banks to drop it.

The Free Checking Account is Profitable

Free checking is profitable for the thousands of community banks and credit unions that continue offering it. There are two primary reasons for this:

- They don’t have the prohibitively expensive branch networks like the mega-banks with their thousands of branches spread across America. The reason free checking isn’t profitable for the big banks is that they allocate these massive branch costs to their checking accounts using the overhead allocation model. In reality, these mega-banks shouldn’t be allocating much, if any, branch costs to their checking accounts. Why? Since the first ATM was deployed in 1969 at Chemical Bank, the big banks have been employing a combination of new technology and punitive pricing (charging customers to use the branch to make a deposit) to keep checking customers out of the branches. The Internet has made visiting the branch obsolete for most checking customers. So, if checking customers are no longer using branches, why should their accounts absorb the overhead costs for them? These fixed costs should be allocated only to the accounts still requiring branches – like CD’s, safe deposit boxes, loans, and investment services.

- By using a different cost allocation model, smaller community banks and credit unions look at adding new checking accounts from a marginal cost perspective – not the “all in cost” perspective of the big banks. Since almost all community banks and credit unions have unused branch capacity and small branch networks, their fixed costs are basically static. So, the revenue from a new free checking account needs only be sufficient to cover variable costs. Any excess revenue can then be applied to the fixed cost base – thereby driving down the fixed cost of all accounts. On the other hand, like the mega-banks, these smaller banks and credit unions shouldn’t be allocating costs to checking accounts when so few checking customers use branches to transact business.

Free checking accounts have been profitable for the community banks and credit unions since they began offering this account in the early 1980s – long before today’s high overdraft fees and lucrative debit card interchange fees. So, it’s disingenuous for today’s mega-banks to claim that recent government meddling in the pricing of overdrafts and interchange fee amounts has made free checking all of a sudden unprofitable.

Remember, the mega-banks didn’t begin offering free checking until they realized the account was wildly popular – even among the wealthy – and wasn’t going away. But, with the recent federal legislation, these big banks saw an opportunity to launch a campaign about free checking profitability in the hopes of forcing the smaller banks to drop this competitive account.

“Free checking is unprofitable and will soon be dead,” is the perfect media story to achieve the mega-banks’ ultimate goal of killing the free checking account. If they can’t have it – they don’t want their competitors having it either. And the mass media had bought into this “big lie” hook, line, and sinker.

The Mega-Banks were the Last to Offer Free Checking

As stated above, the community banks across America were the first banks targeted for the Free Checking and Free Gift program introduced in Lincoln, Nebraska, in 1982. Free checking got a major boost by Washington Mutual (WaMu) when it began its massive expansion program in the Pacific Northwest during the 1990s and into the new century – ultimately expanding to other states around the country. WaMu’s primary marketing focus was on its free checking account. It basically owned the free checking market in the communities it served.

As stated above, the community banks across America were the first banks targeted for the Free Checking and Free Gift program introduced in Lincoln, Nebraska, in 1982. Free checking got a major boost by Washington Mutual (WaMu) when it began its massive expansion program in the Pacific Northwest during the 1990s and into the new century – ultimately expanding to other states around the country. WaMu’s primary marketing focus was on its free checking account. It basically owned the free checking market in the communities it served.

It wasn’t until the late 1990s that the mega-banks reluctantly added free checking to their checking product line. And then, they did very little marketing of the account. Perhaps the most aggressive free checking marketer was Bank of America with its online banner ads. Adding free checking was primarily a defensive move to protect themselves from the aggressive free checking marketing conducted by the community banks and credit unions in all markets where the mega-banks had branches.

We saw how quickly senior management at Chase Bank dropped WaMu’s free checking account shortly after acquiring the bank as a result of the near collapse of our economy. This was done after first promising these customers that Chase would retain free checking.

Blaming this move on recent government legislation is simply a classic example of employing a red herring.

The Truth About Free Checking Can Be Found Here

In the future, should you be writing a blog or media story about free checking, you should consider interviewing senior management and marketing people working for one of the many community banks and credit unions offering the free checking account. They can tell you the true story about free checking and why it is so important for their success.

In addition, you should definitely contact one or both of the financial services vendors specializing in free checking marketing programs. Both are headquartered in Lincoln, Nebraska. One is ACTON Marketing and the other is Haberfeld Associates. Both have been in the free checking business since the early 1980s. They are the true experts when it comes to free checking profitability.